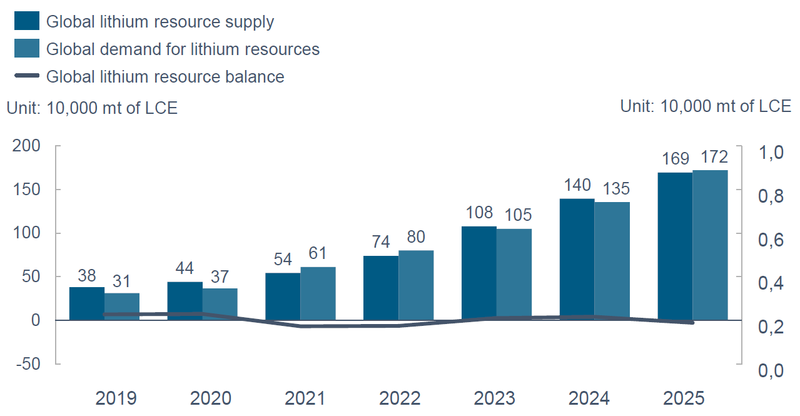

SHANGHAI, Feb 10 (SMM) - Boosted by the global demand for NEVs and the release of the demand in the energy storage market, the global demand for lithium resources will reach about 1.72 million mt of LCE in 2025, with a five-year compound annual growth rate of 33%. The demand will be driven mainly by lithium batteries, while the industry demand will be stable.

On the supply side, with the significant gains in the global lithium salt prices and ore prices, overseas and China’s resource development efforts will increase significantly. It is estimated that by 2025, the global lithium resource output will reach 1.69 million mt of LCE, and the compound annual growth rate will stand at 28%. Lithium extracted from spodumene and salt lakes will contribute to most of the growth.

The global lithium resources presented a supply gap of 9-12% during 2021-2022, and the market mainly worked through inventories due to the insufficient supply of raw materials. From 2023 to 2024, the release of the resources will speed up amid the high lithium prices, and the market may see a small oversupply. In 2025, lithium resources will re-enter a new round of short supply, driven by the boom in the energy storage market.

The short-term resource release will be slow due to the three factors

Lithium extracted from salt lakes: The brine of the salt lakes need to be sun-dried in advance, which will take around two to three years. The efficiency of lithium extraction from brine of overseas salt lakes has improved significantly on the high concentration of lithium. However, potential delays in operations resulting from overseas COVID, employment shortage and inconsistent policies may slow down the release of resources.

Lithium extracted from spodumene: At present, some of the projects under construction by overseas mines are located in Africa and Brazil. There have been delays in the projects due to social factors, and the continued spread of overseas COVID may cause the projects to progress slower than expected. In China, the domestic spodumene concentrate is mainly found in high-altitude and cold areas, bringing about the difficulties in mining operations. Heavy snows will prevent the mining operations in winter, which will slow the entire progress.

Lithium extracted from lepidolite: The mining of the lepidolite mines is still subject to environmental protection supervision, and the capacity expansion is relatively slow.

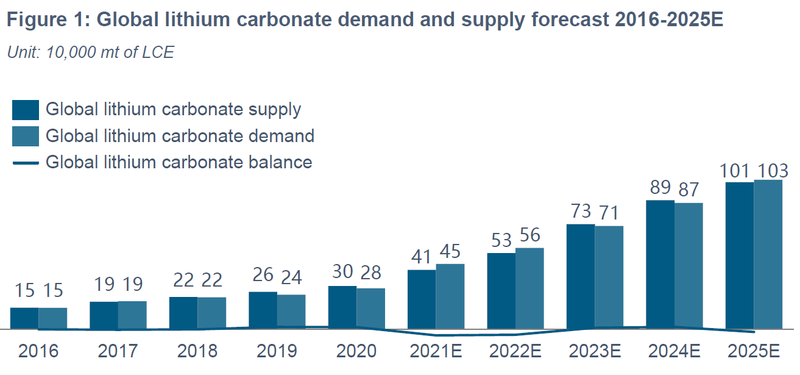

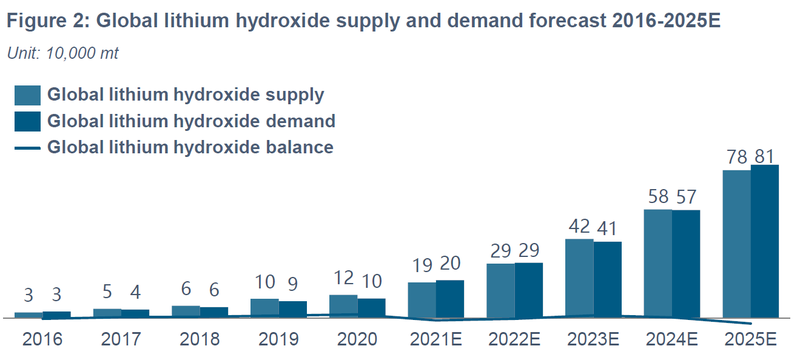

Analysis of global lithium salt supply-demand balance (2016-2025E)

Global lithium carbonate supply increased 37% to 411,000 mt in 2021. Global lithium carbonate capacity rose 23% to 621,000 mt/year. The overseas capacity expansion was mainly contributed by Sociedad Quimica y Minera (SQM); China’s new capacity mainly came from Chengxin Lithium and Lanke Lithium. it is expected that the compound growth rate of global lithium carbonate output will reach 28% in the next five years along with the increase in the lithium carbonate demand from global NEV makers as well as 3C and energy storage fields. The global lithium carbonate supply and demand structure will remain tightly balanced.

Global lithium hydroxide supply increased 53% to 188,000 mt in 2021. Global lithium carbonate capacity rose 22% to 408,000 mt/year. At present, more than 95% of the global lithium hydroxide smelting capacity is located in China, and some new overseas capacity has not yet been put into operation. Therefore, the increase in the output is mainly contributed by the leading domestic smelters. In the future, the demand from NEV makers will increase significantly driven by the market subsidies in the Europe. The domestic high-endurance models will be launched. As such, the demand for lithium hydroxide from global high-nickel batteries and materials will increase significantly. It is expected that the compound growth rate of global lithium hydroxide output will reach 46% in the next five years. The global lithium hydroxide supply and demand will maintain a tight balance.

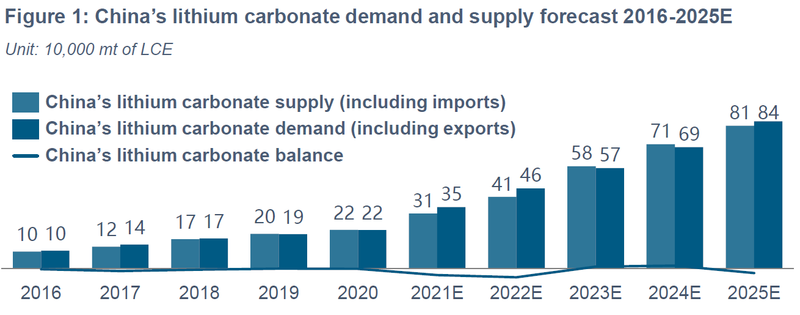

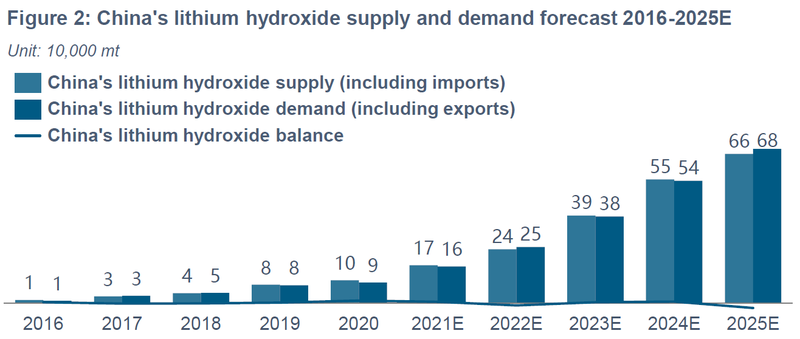

China’s lithium salt supply and demand analysis (2016-2025E)

China’s lithium carbonate supply increased 35% to 229,000 mt in 2021. Domestic lithium carbonate capacity rose 19% to 415,500 mt/year. In terms of raw materials, 49% of China's lithium carbonate output uses spodumene as the feedstock, 25% is produced with lepidolite, and 26% is produced with salt lake brine. The growing supply in 2021 was mainly enabled by lithium salt producers such as Chengxin Lithium, Yin Li New Energy, Lanke Lithium, Hebei Jicheng, Jiangxi Jiuling and Wudi Jinhaiwan Lithium Technology. With the gradual increase in the lithium carbonate demand from power batteries and energy storage batteries, the compound growth rate of lithium carbonate output in China will reach 21.3% in the next five years. In the long run, lithium carbonate will remain in short supply.

China’s lithium hydroxide supply increased 51% to 175,000 mt in 2021. Domestic lithium hydroxide capacity rose 19% to 319,800 mt/year. In terms of raw materials, 89% of China's lithium hydroxide output is produced with spodumene, and 21% is produced with lithium carbonate using the causticising process. Lithium salt companies including Ganfeng Lithium, Tianyi Lithium, Yahua Lithium and General Lithium were among the contributors to the increase in the supply in 2021. It is expected that in the next five years, the compound growth rate of China’s lithium hydroxide output will reach 44.6% as the demand from high nickel batteries and materials gradually increases. In the long run, domestic demand and supply of lithium hydroxide will be tightly balanced.

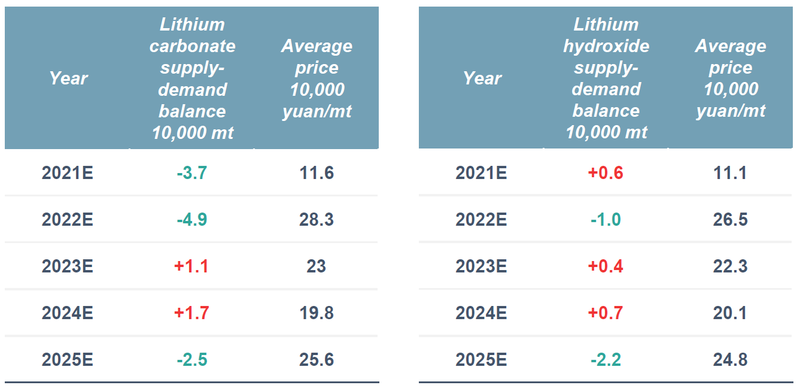

Lithium carbonate price forecast

From 2021 to 2022, the supply of lithium carbonate in China will be restricted by the capacity of overseas resources. There will be a supply gap of around 7% in 2022. The annual average price will rise noticeably to around 280,000 yuan/mt, and the high-end is likely to reach 350,000 yuan/mt.

From 2023 to 2024, most of the new and expanded projects of overseas mines and salt lakes will be put into production, making up for the lithium resources supply shortage. Domestic lithium salt manufacturers will maintain a high operating rate. The growth rate of the NEV market, the largest downstream market for lithium, is expected to be slower than the initial period. The marginal growth of supply will exceed demand, and the lithium carbonate prices are expected to see a brief decline.

The global energy storage market will experience drastic growth in 2025, with NEV sales soaring to 18 million units. The demand for lithium resources will increase significantly. By 2025, the global planned lithium resource projects may face additional bottlenecks, and the supply gap will re-appear. Hence the prices will rise.

Lithium hydroxide price forecast

From 2021 to 2022, NEV subsidies in the Europe are believed to have brought about and will bring about a substantial increase in demand. The export volume of domestic high-nickel batteries and CAMs (cathode active materials) has increased significantly, and the installed capacity of batteries by domestic automakers also surged. China’s demand for high nickel products soared over 50%. The supply side is also restricted by the capacity of overseas resources, but the supply gap is not obvious. As the prices of lithium carbonate rose noticeably, the price difference between lithium carbonate and lithium hydroxide may widen.

During 2023-2024, the demand will be mainly driven by the expansion of overseas battery factories. Export orders for lithium products will increase. The expansion of the leading smelters like Albemarle Chemicals and Ganfeng Lithium will accelerate, with a high concentration ratio of supply. The inventory is likely to grow for a short period of time. The price difference between lithium carbonate and lithium hydroxide will narrow.

In 2025, the demand for lithium hydroxide in China will exceed 400,000 mt, and the amount of imported ore will be relatively limited. The supply gap will re-appear, and the prices will rise.

To access full SMM China Lithium Industry Chain Annual Report 2021-2025, please contact Michael Jiang at michaeljiang@smm.cn or T: +86-21-51666812 |M:+86-1522-1415-920.

![This Week's Key Ex-China Lithium News (3.16-3.20) [SMM New Energy Weekly Ex-China Highlights]](https://imgqn.smm.cn/usercenter/cTxNb20251217171727.jpg)

![[SMM Analysis] This Week's Hydrometallurgy Recycling Market: Salt Prices Fluctuated, and Market Transactions Were Sluggish (2026.3.16-2026.3.19)](https://imgqn.smm.cn/usercenter/WgbTp20251217171727.jpg)